Your essential source for global financial markets information.

Learn More

You want to read about the key facts and developments in global financial markets while optimizing your time.

You are looking for a source without infotainment, triviality, advertisements, and futurology.

You appreciate a minimalist and clear solution to escape noise.

Individual investors, business and financial professionals who value brevity and objectivity.

Independent thinkers who need data and information to build their own views.

Those who want to escape the noise and distraction of endless breaking news, and social media sensationalism.

The essential information on economics, central bank action, corporate deals, and the behaviour of key asset classes: equities, rates, FX, commodities and EM.

Our ‘Global Markets Weekly’ is a proprietary online report in English, published on Sundays.

Try

it for free.

Accurate, brief, factual and reliable content.

Episode Sunday 3, Dec. Get started to see last episode

Bonds Rally on Lower Inflation

The latest inflation data in the US and the Eurozone confirms an acceleration of the disinflation trend, leading to investors' bets that the tightening cycle is beginning to reverse. Despite warnings by central bankers that the battle against inflation is far from over and demands for a cautious approach, bond markets rallied, stocks advanced for a fifth consecutive week, and gold jumped to a record high.

Economic data in developed economies are having a stronger impact on markets than updates on geopolitical conflicts in the Middle East and Ukraine. Investors are anticipating a change in the interest rate outlook and are pricing in the peak of a two-year cycle. The risk-on sentiment is reflected in the VIX index, which dropped to the lowest level since the start of the pandemic, closing at 12.6%, nine figures lower year-to-date as the S&P 500 gained 19.7% in the same period.

• Crude oil prices fell 2% after OPEC+ finally held their postponed meeting to determine the extension of voluntary output cuts. Gold rallied 3.4% to its all-time nominal record of $2,071.

• Chinese stocks continue to decline following mixed data releases, and the crypto sector remains strong, with Bitcoin reaching an 18-month high of just under $40,000.

• Israeli troops have resumed their attacks on Hamas after the hostage-for-prisoners exchange a few days ago. Israel is planning for a long war against terrorism that could last for at least one year. Washington accused Turkey of facilitating access to international funding for Hamas.

Copyright © 2023 Succinct Information and/or its affiliates. All rights reserved.

Monetary Policy

There were three policy meetings in developed economies last week. The Reserve Bank of New Zealand kept rates unchanged at 5.5% as policymakers consider that inflation remains too high (5.6%), and interest rates should be maintained at restrictive levels. The RBNZ signalled that if inflationary pressures did not ease, the OCR rate would likely need to be increased further. The central bank’s target inflation rate is a 1-3% range.

The Bank of Korea also held its policy rate steady at 3.5% and signalled it will remain at the current level as inflation persists. The BoK upgraded next year’s inflation forecast to 2.6% and reduced its growth estimate to 2.1% for 2024. Inflation is running at 3.8%, still above the 2% target.

"It means we are going to take enough time until we are sure that inflation has sufficiently converged - it could be six months but realistically I'd say it's likely to be longer than that," Governor Rhee Chang-yong said.

Inflation Continues to Decline

• Eurozone inflation dropped far more than anticipated in November to 2.4% YoY, the lowest reading since mid-2021, raising expectations that the ECB’s tightening cycle is near its peak. Inflation declined from October’s 2.9% print, mainly due to lower energy prices and stable food and services prices, with Italian consumer prices falling the most to 0.7%, and Germany’s easing to 2.3%, below the bloc’s average.

Core inflation also fell to 3.6% from 4.2% a month earlier, an indicator of key importance to ECB’s policymakers. President Lagarde warned that wage pressures remained strong and that victory against high inflation was far from over as the target is still 2%.

• Inflation in the US is also cooling with PCE (personal consumption expenditures) prices unchanged in October, following a 0.4% rise in September. On an annual basis, headline PCE inflation rose by 3.0%, much lower than the 3.4% recorded a month earlier. Core PCE, the Fed’s preferred inflation gauge, also decelerated to 3.5% YoY. The Super Core PCE measure, which is PCE services minus energy and housing, rose by 3.9%, also cooler than a month earlier.

The latest data on the labour market, a closely watched indicator by the Fed, is gradually easing with a small uptick in jobless claims. Next week’s monthly employment report will be key. Despite a clear disinflationary trend, central bankers were cautious about mentions regarding the timing of interest rate cuts.

Interest Rates $

$

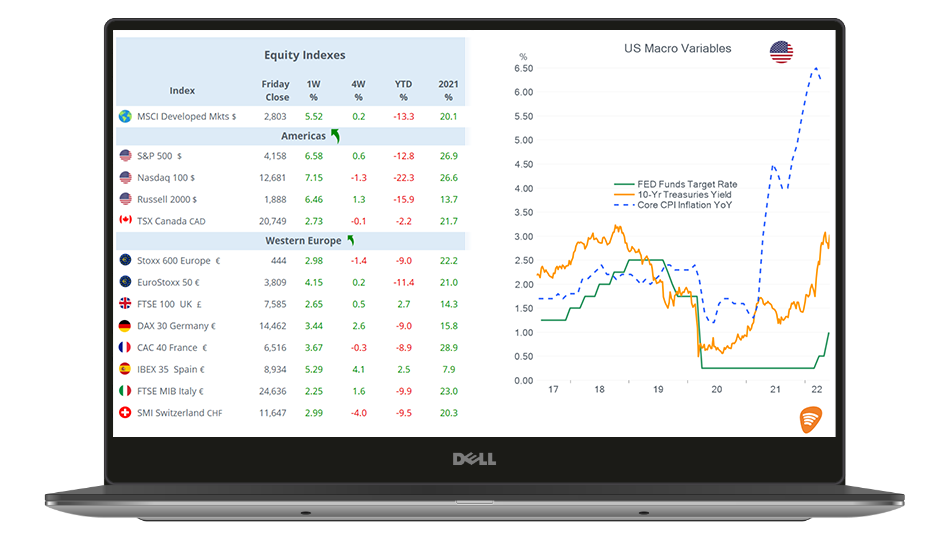

The inflation readings in the US and the Eurozone triggered strong demand for bonds, sending yields sharply lower. The disinflation trend was confirmed by last week’s updates, and investors responded with bets on fixed-income securities despite central bankers warning that it is too early to claim victory against inflation. Bond yields fell across tenors in every developed market.

The yield on 2-year US Notes declined by 39 basis points to 4.57%, while 10-year Treasuries closed 26 basis points lower at 4.22%, its lowest closing level in three months. 10-year TIPS, inflation-protected Treasuries, are yielding 2.0%, 41 basis points more than at the end of last year. The TIPS yield curve is reasonably flat, with 5-year bonds at 2.01% and 30-years at 2.11%. German government bonds saw similar moves with a steep drop in yields, but all leading curves in advanced economies remain in inverted mode.

• Fitch upgraded Greece on Friday (after market close) to investment grade (BBB-) due to a favourable debt-servicing structure and a notable decline in general government debt. S&P also rates Greece at BBB-, and Moody’s maintains a sub-investment grade rating at Ba1.

• The Dollar index was almost unchanged, showing mixed performance for major currency pairs. The Euro fell by half a per cent, cable appreciated by almost 0.8%, and the yen and the Kiwi dollar rallied around 2% last week.

The notable mover was gold, which climbed by 3.4% to close at $2,071, its highest level on record, driven by the outlook for interest rates. Additionally, the World Gold Council reported that central banks bought 800 tonnes of physical gold in the first nine months of the year, a 14% year-on-year increase, with China’s PBoC being the largest buyer.

Commodities

On Thursday, following a delay of the OPEC+ meeting due to members’ differences, the group agreed to voluntary output cuts totalling around 2.2mbpd for early next year led by Saudi Arabia. Crude oil prices fell on the week as traders doubted the efficiency of the measure as the reduction was voluntary.

OPEC+ members account for more than 40% of global supply with 43mbpd, and the voluntary production cuts account for a total of 5mbpd. The decision to lower supply is aimed at supporting prices and stabilising the market after a 7% fall in the past four weeks. OPEC+ invited Brazil to join the group and an answer is expected soon.

In other energy markets, European gas prices fell almost 7% last week despite colder weather conditions as underground storage facilities were 97% full at the end of November, 12% higher than the five-year average. Ample supply pulled spot prices lower to close the week at €43.5/MWh.

• Corn futures fell to a three-year low on the back of increased supply from Brazil and the US and weak global demand. US farmers increased the size of corn acreage at the start of the year following strong prices at the end of 2022, but demand during 2023 has not risen enough to justify higher prices. On average (several futures contracts) corn has fallen 15% this year.

• Coffee ‘C’ Arabica futures rallied almost 10% as data showed that inventories fell to a 24-year low of 224k bags. Coffee and cocoa inventories in EU warehouses are at risk of destruction due to a deforestation law implemented earlier this year. The law’s goal is to limit agricultural commodities harvested in regions where deforestation is not allowed. The countries concerned include Brazil, Vietnam, and Colombia for coffee plantations and Ivory Coast and Ghana for cocoa beans. Coffee’s March contract on the ICE US exchange closed at 184.3 cents per pound, a six-month high.

Upward Momentum Persists

Developed stock indexes traded firmer, with the S&P 500 gaining for a fifth consecutive week and value names outperforming growth companies. The Dow Jones Industrials rose by 2.4% last week to the highest level in nearly two years. The Nasdaq Composite and the S&P 500 indexes had their best month in November since mid-2020 with a 10.7% and 9% rally, respectively. Europe’s broad Stoxx 600 had its best month since January with a 6.5% rise, and the Dax and Ibex were the best-performing country indexes.

The improved outlook for a lower interest rate environment led to a strong performance for property stocks, with Real Estate as the best-performing sector, rising by 4.7%. The weakest sector of the week was Communication Services, with a 2.5% drop, mostly on Meta’s 4% and Google’s 3.5% decline.

• Salesforce (software vendor, market cap $254bn, P/E 99x) met revenue expectations ($8.72bn, +11% YoY) and beat earnings estimates ($1.22bn, a six-fold rise YoY) when it reported Q3 results last week. CRM has been successful in lowering costs as part of a restructuring plan and raised its 2024 forecast for operating cash flow growth to 33%, projecting a 10% surge in revenue for Q4.

Shares rallied 16% last week, marking its best week in more than three years, reaching $260, the highest level in two years.

-

-

-

-

M&A: Pharma

---

---

• AbbVie Inc (US, pharmaceuticals, mcap $253bn, P/E 39x) agreed to acquire ImmunoGen Inc (US, biotechnology, mcap $7.85bn) for $8.4bn in cash and a total enterprise value of $10bn. Terms: $31.26 per share, representing a premium of 95% to the stock's previous close.

AbbVie’s interest is in ImmunoGen's Elahere drug which is part of a new class of treatments called antibody-drug conjugates (ADC) that specifically targets cancer cells, potentially reducing toxicity for other cells. Elahere generated $212mn in revenues for the first three quarters of the year and is expected to become a blockbuster drug by the end of this decade.

Asset Divestiture: Airports

• Ferrovial (Spain, Netherlands-listed, infrastructure, mcap €23.3bn, P/E 142x) agreed to sell all of its 25% stake in Heathrow, London’s busiest airport for £2.4bn. Ferrovial relisted from Madrid to Amsterdam in June 2023 and started trading at €28. Shares closed at €31.85 on Friday. The asset sale triggered interest in other airports by other global infrastructure groups including GIP and Macquarie.

Bankruptcy: Property

• Signa Holding (Austria, real estate, privately owned), owner of almost every department store in Germany, half of the Chrysler Building in NY and a partner in London’s Selfridges filed for self-administration in Austria on Wednesday. It is expected to be a complex corporate restructuring due to the multiple cross-shareholding companies and trusts involved. Austrian bankruptcy law allows for an internal restructuring attempt without having to delegate the management to an external administrator.

Several European banks have an exposure of €13bn to Signa’s web of entities with Julius Baer having reported a $655mn exposure and Raiffeisen Bank of $800mn. The group has three months to present a plan to credits, according to Austrian corporate law.

LBO: Pet Care Services

• Rover Group (US, online pet marketplace, mkt cap $1.98bn, P/E 194x) agreed to be taken over by private equity Blackstone for $2.3bn in cash. Rover’s biggest shareholders include Foundry Group, Madrona Ventures, Menlo Ventures and True Wind Capital. Terms: $11 per share, a premium of 30% from the last close price.

Rover Group runs an online marketplace where pet care providers offer services such as dog walking and in-home pet sitting. It became a publicly listed company in July 2021 after being acquired by SPAC Nebula Caravel Acquisition Corp and shares jumped to $14 when that deal was announced.

Rover reported sales of $217mn and profits of $11mn in the LTM.

Revaluation: Social Media

• Social media platform X, formerly Twitter, valued its equity at $19bn only a year after Elon Musk paid $44bn for the company, X informed employees under its stock compensation plan. Banks that financed the deal include Bank of America, Morgan Stanley, Barclays, MUFG, BNP, and SocGen and are sitting on paper losses amounting to several billion dollars. X has 245mn daily active users and expects to return to profit in Q1’24.

Potential IPO: Sneakers

• Golden Goose, the Italian luxury sports shoe brand owned by private equity Permira is planning an IPO in Milan that could value the firm at €3bn. Permira acquired the Venice-based company in 2020 for €1.3bn from rival Carlyle.

Crypto assets continue to trade firmer driven by the recent positive momentum behind the applications for the first spot Bitcoin ETF in the US as well as the expectations that interest rates are at their peak. Bitcoin is 4% higher week-to-date at its highest level in 18 months, having broken the 39,000 threshold for the first time since its collapse in May 2022. The total market cap of the sector stands at $1.48tn, also the highest since the crypto winter of last year when the Terra ecosystem failed.

Meme coin DOGE was last week’s best performer with a nearly 10% jump for a market value of $12bn, namely on Elon Musk’s attitude toward tech giants on their decision to stop advertising on ‘X’.

Stocks in emerging markets traded mixed with Chinese and Russian markets underperforming those in India, Brazil and Mexico. On average, the asset class ended the week flat compared to solid gains in advanced economies. China’s CSI300 index lost 1.6% and Hong Kong’s Hang Seng plunged 4.2% while Russia’s Moex index declined by 2.3%

China’s latest economic activity levels highlighted the loss of positive momentum with the manufacturing PMI dropping for the second straight month. Authorities are implementing a 25-point plan to provide financial support to the private sector aimed at improving business confidence. Also, the central bank announced a change in the dynamics of lending to improve the efficiency and structure of loans.

• Russia saw the rouble depreciate 2.1% to 91.22 and accumulated a decline of 20.5% year-to-date. Moscow acknowledged that the economic sanctions against the country by the US and its allies will last for several years. Russia’s oil and gas export revenues, a significant income of hard currency for the Kremlin, fell 41% in the first nine months of the year.

Russia’s 2035 dollar bond widened 21bp last week to 1,470bp over Treasuries, for a 19% yield and has widened 50bp in the past four weeks.

• Turkey’s rating outlook was upgraded by S&P Ratings from B stable to B positive. Moody’s rates Turkey at B3 with a stable outlook. 10-year dollar bonds widened 10bp to +390bp for an 8.11% yield at 89.3 bid price. 10-year domestic bonds in Lira are yielding 24% compared with 10% at the end of last year and inflation running at 60%.

• Yesterday, The Philippines was hit by a powerful earthquake of at least magnitude 7.5 in the Southern Mindanao region, followed by several after-shocks of at least 6.0. The incident triggered tsunami alerts across the South Asian Sea that were later lifted.

Mon 4 - Sun 10